March Market Review

It really depends on how you look at things

Executive Summary

Can’t stop, won’t stop: Despite challenging macro conditions, including inflation at 5 percent, continued interest rate hikes by the Federal Reserve, and the two biggest bank failures in US history, equities continued their upward trend—the resilience of the market is noteworthy.

Bank Failures: The Federal Deposit Insurance Corporation (FDIC) recently took over two banks, Silicon Valley Bank and Signature Bank of New York, as they were placed into receivership. These are the first bank failures since 2020 and the second and third largest in US history.

The Federal Reserve hikes again: During the latest Federal Open Market Committee meeting, the Federal Reserve decided to increase the Fed Funds rate for the ninth consecutive time. They highlighted that recent indicators demonstrate a modest increase in spending and production. Additionally, they stated that the job market remains strong with low unemployment, but inflation is still high. The new Fed Funds Rate has been set to range between 4.75 and 5.00 percent.

Can’t stop, won’t stop: Despite challenging macro conditions, including inflation at 5 percent, continued interest rate hikes by the Federal Reserve, and the two biggest bank failures in US history, equities continued their upward trend—the resilience of the market is noteworthy.

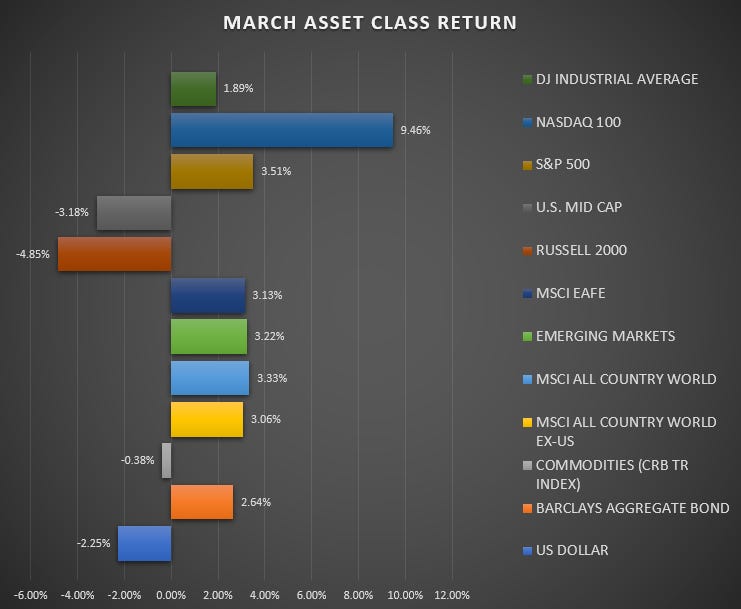

In March, the second and third largest bank failures in the US led to mid-month turmoil, prompting investors to seek refuge in large-cap technology companies as a safety trade. This resulted in significant gains for the NASDAQ 100 index, which saw an impressive +9.46 percent increase.

The surge in stock prices for companies like AAPL, GOOGL, MSFT, NVDA, AMZN, and META can be attributed to fears of an economic slowdown due to credit tightening and the sharp decline in Treasury US yields. Investors reflexively herded into these companies, which had outperformed during the last economic cycle characterized by slow growth and low interest rates.

While the S&P 500 climbed by +3.5 percent and the Dow Jones Industrial Average rose by +1.9 percent, small (-4.85%) and mid-cap (-3.2%) US companies experienced notable declines. These declines were likely due to the failures of Silicon Valley Bank and Signature Bank of New York, which disproportionately affected small and mid-sized companies relying heavily on regional banks for capital access. The tightening of credit standards and decreased credit availability pose significant challenges for these companies in the upcoming quarters, and investors seem to be pricing this in.

International equities saw consistent gains across the board, with the MSCI EAFE experiencing a rise of +3.1 percent, the Emerging Markets increasing by +3.2 percent, and the All Country World Index and All Country World Index ex-US adding +3.3 percent and +3.0 percent, respectively.

Bonds rallied as yields fell across the curve, with the Barclays Aggregate Bond Index rising +2.6 percent; commodities were essentially unchanged in March, while the US Dollar declined -2.2 percent.

The first quarter year-to-date returns show that the tech-dominated NASDAQ 100 outperformed other indices, experiencing a significant gain of +21.3 percent in March. In contrast, the Dow Jones Industrial Average was underperforming compared to the S&P 500.

It is worth noting that last year, the NASDAQ 100 underperformed the S&P 500, declining by -33 percent compared to the S&P 500's -19 percent decline, while the Dow Jones outperformed the S&P 500 with a modest decline of only -9 percent. Whether the first-quarter returns are simply mean-reverting from last year or a re-establishment of the trend over the past decade remains to be seen. While I am in the mean-reversion camp, I remain open-minded.

Bank Failures: The Federal Deposit Insurance Corporation (FDIC) recently took over two banks, Silicon Valley Bank and Signature Bank of New York, as they were placed into receivership. These are the first bank failures since 2020 and the second and third largest in US history.

The immediate cause of these failures was a sudden outflow of electronic deposits due to concerns over each bank's financial stability. These concerns were further amplified when Silicon Valley Bank announced the sale of $21 billion worth of bonds and a secondary offering of $2.1 billion in equity to strengthen its balance sheet.

Once the news of Silicon Valley Bank's plans to shore up its balance sheet became public, depositors swiftly moved uninsured deposits to larger money-center banks deemed systemically important. The reasoning was that the Federal Government would backstop uninsured deposits left in Systemically Important Banks (SIB).

The repercussions were immediate, as the S&P Bank Index (KBE) dropped by -20 percent over the next three trading days.

Although it is too soon to determine the long-term effects, Silicon Valley Bank and Signature Bank of New York appear to be outliers. The US banking system is more robust thanks to policies implemented after the Great Financial Crisis.

The Federal Reserve hikes again: At the latest Federal Open Market Committee meeting, the Federal Reserve raised the Fed Funds rate for the ninth consecutive time. They noted that there had been a slight uptick in spending and production, and the job market remains robust with low unemployment, although inflation remains high. The new Fed Funds Rate range is set between 4.75 and 5.00 percent.

The March Summary of Economic Projections (SEP) reveals that the Fed's projections have hardly changed since their December 2022 meeting.

The Fed has kept the terminal Fed Funds Rate (FFR) steady at 5-5.25 percent, with a slight positive growth projection for real GDP in 2023, while inflation remains high and unemployment is predicted to increase.

Looking ahead, the Federal Open Market Committee is scheduled to meet on May 2-3, with futures markets suggesting a 68 percent probability of a 25 basis point rate hike, reaching the Fed’s target range of 5-5.25 percent. Although investors anticipate interest rate cuts in the latter half of the year, the Federal Reserve intends to maintain a high interest rate for an extended period. It remains to be seen who will yield first.